What to Do If Someone Steals Your Banking Information

Discover how to protect your accounts after a banking data breach

Discovering that your banking information has been compromised is a heart-sinking moment. Whether you noticed a strange charge on your statement or received an alert about a login from an unknown device, the clock starts ticking the moment your data is out in the open.

In the digital age, financial security is a moving target. However, having your information stolen doesn’t have to result in financial ruin. By taking swift, strategic action, you can mitigate the damage, recover lost funds, and fortify your accounts against future attacks. This guide outlines the exact steps you need to take to reclaim your financial security.

Critical First Steps: What to Do the Moment Your Banking Info is Compromised

The first 24 to 48 hours after discovering a breach are the most vital. The goal is to “stop the bleed” before the unauthorized user can drain your accounts or open new lines of credit in your name.

1. Contact Your Financial Institution Immediately

Your bank or credit union should be your first phone call. Do not wait for the business day to begin; most major banks have 24/7 fraud departments.

-

Request a Freeze or Close the Account: Ask the bank to freeze your current accounts or, if necessary, close the compromised account and open a new one with a different account number.

-

Report Specific Transactions: Point out exactly which charges were not authorized by you.

-

Request New Cards: If your debit or credit card info was stolen, have them cancel the old cards and mail new ones with updated CVV codes.

2. Change Your Digital Credentials

If a hacker gained access to your banking information through your online portal, they likely have your password.

-

Update Passwords: Change your banking password immediately. Ensure it is a “strong” password—at least 12 characters, including symbols, numbers, and a mix of cases.

-

Update Your Email Password: Often, hackers get into banks by first compromising the user’s email. If they control your email, they can “reset” your bank password without you knowing.

-

Enable Multi-Factor Authentication (MFA): If you don’t have it already, enable MFA (or 2FA). This requires a code from an app or a text message in addition to your password, providing a second layer of defense.

Navigating the Legal and Reporting Process: Who to Notify

Once the immediate threat is contained, you need to create a formal paper trail. This protects you legally and is often required by banks to process fraud claims.

1. File a Report with the Federal Trade Commission (FTC)

In the United States, the FTC is the primary body for tracking identity theft. Visit IdentityTheft.gov.

-

This site will help you create an Identity Theft Report.

-

This official document is essential when dealing with credit bureaus and debt collectors later on.

2. Place a Fraud Alert on Your Credit Reports

There are three major credit bureaus: Equifax, Experian, and TransUnion. You only need to contact one of them to place a “Fraud Alert” on your file; by law, that bureau must notify the other two.

-

Initial Fraud Alert: This lasts for one year and makes it harder for someone to open a new account in your name, as businesses must verify your identity before issuing credit.

-

Credit Freeze: For maximum security, consider a full credit freeze. This prevents anyone (including you) from opening new credit accounts until you “unfreeze” it with a PIN.

3. Contact Local Law Enforcement

While local police may not be able to “catch” a digital hacker across the globe, filing a police report provides you with a case number. This is often required by insurance companies or if you need to dispute large sums of money.

The Road to Recovery: Disputing Fraudulent Charges and Recovering Funds

Under U.S. law, specifically the Electronic Fund Transfer Act (Regulation E), your liability for unauthorized electronic transfers is limited, provided you report them quickly.

Understanding Your Liability

-

Reported before any charges: $0 liability.

-

Reported within 2 business days: Maximum $50 liability.

-

Reported between 2 and 60 days: Maximum $500 liability.

-

Reported after 60 days: You could be liable for the entire amount lost.

How to Properly Dispute a Transaction

When you speak to the bank’s fraud department, follow up in writing. Send a certified letter that includes:

-

Your account number.

-

The date and dollar amount of the fraudulent transaction.

-

A brief explanation of why you are disputing it.

-

A copy of your FTC Identity Theft Report.

Advanced Digital Hygiene: How Your Information Gets Stolen

To prevent a second occurrence, it is important to understand the sophisticated methods used by modern cybercriminals.

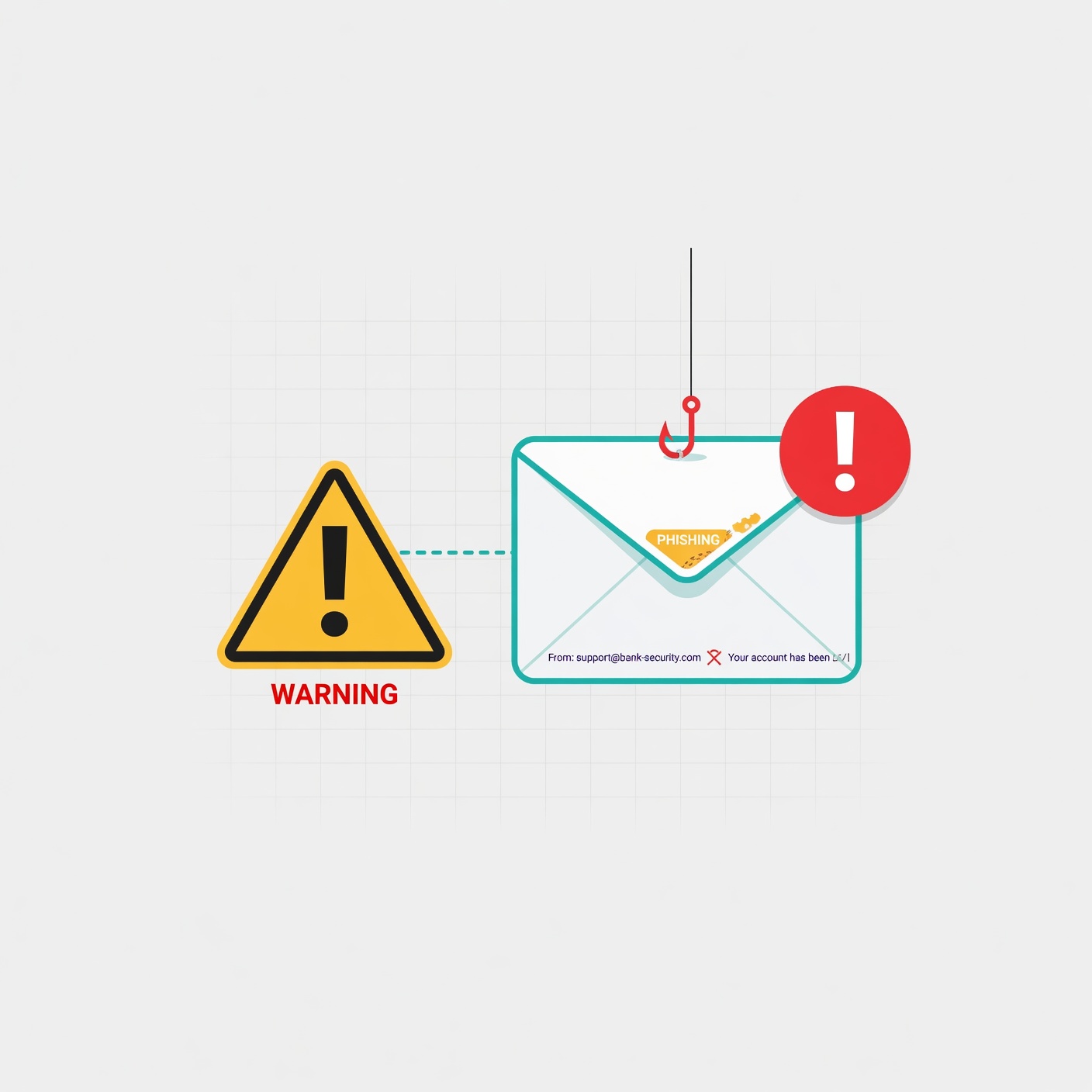

Phishing and Smishing Campaigns

Phishing involves fraudulent emails, while “smishing” uses SMS text messages. These messages often look like official bank alerts, claiming there is a “problem with your account” and providing a link. Once you click and “log in,” the hacker has your credentials.

-

The Rule: Never click links in unexpected texts or emails. Always go directly to the bank’s official website or app.

Card Skimmers and Shimmers

Skimmers are physical devices placed over credit card readers at gas pumps or ATMs. They read the magnetic stripe of your card. “Shimmers” are newer, thinner versions that can read data from the EMV chips in your card.

-

Prevention: Use contactless payments (like Apple Pay or Google Pay) whenever possible, as they use “tokenization” which never reveals your actual card number to the terminal.

Credential Stuffing and Data Breaches

If you use the same password for your Netflix account as you do for your bank, you are at risk. When a minor website suffers a data breach, hackers take those email/password combinations and try them on major banking sites. This is known as “credential stuffing.”

Long-Term Financial Fortification: Building a Bulletproof Defense

Recovery is about more than just getting your money back; it’s about ensuring it never happens again.

1. Use a Dedicated Device for Banking

If possible, do your online banking on a device that you don’t use for general web surfing or downloading games. A “clean” tablet or laptop reduces the risk of malware or keyloggers recording your keystrokes.

2. Monitor Your Statements Weekly

Don’t wait for the end of the month to check your statement. Spend five minutes every Sunday reviewing your transactions. Small “test” charges of $0.99 or $1.00 are often used by hackers to see if a card is active before they make a large purchase.

3. Review Your Credit Report Annually

You are entitled to a free credit report from each of the three bureaus every year via AnnualCreditReport.com. Look for accounts you didn’t open or inquiries from companies you don’t recognize.

4. Consider Identity Theft Protection Services

Services like Aura or LifeLock monitor the “dark web” for your information and provide insurance to cover legal fees if your identity is stolen. For individuals with high net worth or complex financial lives, this peace of mind is often worth the monthly subscription.

The Emotional Impact of Financial Theft

It is important to acknowledge that having your banking information stolen is a violation of your privacy and can cause significant stress. It is common to feel anxious or hyper-vigilant after a breach.

-

Stay Organized: Keep a folder (physical or digital) with all your correspondence, case numbers, and notes from phone calls. Organization reduces the feeling of chaos.

-

Know Your Rights: Remember that as a consumer, you have strong protections. In the majority of cases, as long as you act quickly, you will not be held responsible for the lost funds.

Final Checklist for Your Financial Security

| Action Item | Frequency | Importance |

| Change Banking Password | Every 90 Days | High |

| Check Account Balance | Daily/Weekly | Critical |

| Review Credit Score | Monthly | Medium |

| Update Software/OS | As available | High |

| Enable Push Notifications for Charges | Once | Critical |

By following this roadmap, you transform from a victim into a proactive guardian of your wealth. Financial security is not a one-time setup; it is a continuous practice of awareness and action. Stay vigilant, use the tools available to you, and always trust your gut if a transaction or a communication feels “off.”