Understand how social media can make you spend money

How algorithms and advertising shape your purchasing decisions

In the modern era, the marketplace is no longer a physical destination we visit; it is a permanent resident in our pockets. Every time we unlock our phones to “just check a notification,” we are entering a highly engineered environment designed to separate us from our money. Social media platforms—once simple tools for connection—have evolved into the most sophisticated sales engines in human history.

While we often blame ourselves for a lack of willpower, the truth is that we are participating in an asymmetrical war. On one side is your individual brain; on the other side are multi-billion dollar algorithms and thousands of behavioral psychologists working to trigger your next impulsive purchase. Understanding the mechanics of this “Attention-to-Transaction” pipeline is the first step in reclaiming your financial sovereignty.

The Dopamine Trap: Why Your Brain Craves the “Buy Now” Button

To understand why social media makes you spend, we have to look at the brain’s reward system. The primary chemical at play here is dopamine. Contrary to popular belief, dopamine isn’t about the pleasure of receiving a product; it’s about the anticipation of the reward.

The Feedback Loop of Scrolling

Social media is designed around a “variable reward schedule”—the same psychological mechanism found in slot machines. You scroll through your feed, never knowing if the next post will be a funny video, a friend’s update, or a perfectly targeted ad for a pair of shoes you didn’t know you needed. This uncertainty keeps the dopamine flowing.

When you finally see a product that resonates with your aesthetic or lifestyle, your brain experiences a “spike.” The act of clicking “Add to Cart” provides a temporary sense of achievement and relief from the “search” tension. By the time the package arrives, the chemical high has usually faded, leading to “buyer’s remorse”—and the urge to start scrolling again for the next hit.

Algorithms of Desire: How Platforms Predict Your Next Purchase

You might think it’s a coincidence that you were just talking about wanting a new espresso machine, and suddenly your Instagram feed is full of them. It isn’t magic, and contrary to some conspiracy theories, they don’t even necessarily need to “listen” to your microphone. They have something much more powerful: Data.

Predictive Modeling and Micro-Targeting

Every “like,” every second you spend hovering over a photo, and every link you click is fed into a machine-learning model. These algorithms know your income bracket, your relationship status, your insecurities, and your aspirations.

They don’t just know what you want; they know when you are most likely to buy it. If the data shows you tend to make impulsive purchases on Friday nights after a stressful week, the most tempting ads will be served to you at exactly 8:00 PM on Friday. You aren’t just seeing ads; you are being served personalized temptations at your most vulnerable moments.

The Influencer Paradox: From Inspiration to Impulsion

In the early days of advertising, we saw celebrities on billboards. We knew they were being paid to sell us a car or a perfume. Today, that line has blurred. Influencers have replaced celebrities as the “trusted friends” of the digital age.

The Illusion of Authenticity

We follow influencers because we feel a “parasocial” connection to them. We watch them cook in their kitchens, play with their kids, and share their daily struggles. This creates a sense of trust. When an influencer says, “I’ve been using this skincare routine and it changed my life,” our brains process it as a recommendation from a friend, not a commercial.

The “Aspirational Identity” Trap

Influencers don’t just sell products; they sell identities. We don’t buy the $200 yoga mat because we need a mat; we buy it because we want to be the kind of person who is as disciplined, glowing, and balanced as the person on the screen. Social media allows us to “purchase” a fragment of that identity instantly, even if we never actually do the yoga.

Social Comparison and the High Price of “Clout”

Humans are evolutionary hardwired to compare themselves to their peers. In the past, this was limited to the “Joneses” next door. Now, we are comparing our “behind-the-scenes” reality to the “highlight reels” of everyone else in the world.

The FOMO (Fear of Missing Out) Economy

FOMO is a powerful financial driver. When we see our friends—or even strangers—traveling to Bali, dining at Michelin-star restaurants, or unboxing the latest tech, we feel a sense of lack. This “Relative Deprivation” triggers a need to spend to “keep up.” We use money as a tool to signal that we are also successful, adventurous, and relevant.

Status Anxiety and Revenge Spending

“Revenge spending” often occurs when we feel frustrated or stagnant in our own lives. If we can’t afford a house or a major career promotion, we might spend $1,000 on designer clothes or a high-end gadget to prove to our digital “tribe” (and ourselves) that we are still doing well. It is a temporary band-aid for a deep-seated social anxiety, and it almost always ends in a credit card debt hangover.

The Rise of Frictionless E-commerce: Buying in One Swipe

The distance between “want” and “bought” has never been shorter. In the past, you had to get in a car, drive to a store, find the item, and stand in line to pay. These “friction points” allowed your logical brain (the prefrontal cortex) to catch up and ask, “Do I really need this?”

Instagram and TikTok Shops

Platforms have now integrated the storefront directly into the feed. With “Instagram Shop” or “TikTok Shop,” you can buy a product without ever leaving the app. Saved credit card information and biometric payments (FaceID) mean that a $500 purchase can happen in less than two seconds.

By eliminating the time to think, platforms have eliminated the time to say “no.” This gamification of spending turns your financial resources into just another “point total” in an app, making the loss of money feel less real until the bill arrives at the end of the month.

Artificial Scarcity: The Psychological Warfare of “Last Chance” Deals

Social media is the perfect environment for “Dark Patterns”—design choices intended to trick users into making decisions they didn’t intend to make.

Manufacturing Urgency

Phrases like “Limited Edition,” “Only 2 left in stock!”, or “Flash Sale ends in 02:45:12” are often used to trigger a “fight or flight” response. When the brain perceives scarcity, it shifts from analytical mode to survival mode. In this state, the fear of “missing out” on a deal outweighs the logical concern for your bank account. You aren’t buying the item because it’s useful; you’re buying it because your brain wants to stop the “anxiety” of losing the opportunity.

The Hidden Financial Cost: Opportunity Cost in a Digital World

The danger of social media spending isn’t just the $50 here or the $100 there. It is the Opportunity Cost—the wealth you could have built if that money had been invested instead of spent.

The “Scroll Tax” and Compound Interest

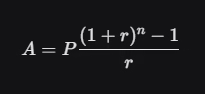

If a person spends $200 a month on impulsive purchases triggered by social media, they aren’t just losing $2,400 a year. If they had invested that $200 a month in a diversified index fund with a 7% average annual return, look at the “Wealth Gap” over time:

-

In 10 years: $34,000

-

In 20 years: $100,000

-

In 30 years: $240,000

The formula for this growth is the compound interest equation:

(Where A is the final amount, P is the monthly contribution, r is the monthly interest rate, and n is the number of months.)

Every “clout-driven” purchase is a direct theft from your future self. By the time you reach retirement age, that “must-have” trending gadget from 2026 could have been a significant portion of your house down payment or your retirement fund.

Digital Hygiene: 5 Steps to Protect Your Wallet from Your Phone

You don’t have to delete your social media accounts to save your finances. You just have to re-introduce the “friction” that the platforms worked so hard to remove.

1. The 48-Hour Cart Rule

Never buy an item the first time you see it on social media. Add it to your cart, and then close the app. Force yourself to wait 48 hours. Usually, the dopamine spike will subside, and you will realize the “need” was actually just a temporary chemical urge.

2. Unsubscribe and Unfollow

Your feed is your environment. If you follow accounts that constantly showcase luxury hauls or “must-have” products, you are living in a digital mall. Unfollow influencers who trigger your FOMO and unsubscribe from retail marketing emails. If you don’t see the “deal,” you won’t feel the need to spend.

3. Turn Off “One-Click” Payments

Delete your saved credit card information from your browser and your favorite apps. Forcing yourself to get up, find your wallet, and manually type in 16 digits provides a crucial “cooling off” period. This small act of friction can stop up to 80% of impulsive purchases.

4. Set App Limits

Platform algorithms are designed to keep you on the app as long as possible (the “doomscroll”). The longer you stay, the more ads you see. Use your phone’s built-in settings to limit your social media time to 30 or 60 minutes a day. Less time on the app equals less exposure to temptation.

5. Create a “Fun Money” Bucket

Complete deprivation often leads to a “spending binge.” Instead, allocate a small, fixed amount each month to “guilt-free” impulsive spending. Once that bucket is empty, you are done for the month. This gives you the freedom to enjoy your money without sabotaging your long-term goals.

Reclaiming Your Financial Sovereignty in the Age of Attention

In a world that profit off your impulsivity, the most radical financial act you can perform is to be intentional. Social media is a tool, but currently, for many people, the tool is using them.

Financial stability isn’t just about how much you earn; it’s about how much you keep. By understanding the dopamine loops, the algorithmic targeting, and the social pressures of the digital age, you can move from a “reactive” spender to a “proactive” saver. Your bank account should reflect your values and your future, not the quarterly earnings goals of a social media giant.

Stop letting a glass screen dictate your net worth. The next time you feel the “urge” to click that ad, take a breath, lock your phone, and remember: The best deal of all is the one where you keep your money.