See the comparison of saving versus investing

Learn When to Save, When to Invest, and How to Balance Both

In the journey toward financial freedom, two words are often used interchangeably, yet they represent entirely different worlds of money management: Saving and Investing.

Understanding the nuances between these two strategies is more than just a lesson in vocabulary; it is the foundation of your wealth-building architecture. In 2026, with the global economy shifting and inflation remaining a persistent topic of conversation, knowing when to keep your cash in a “fortress of safety” and when to put it into the “engine of growth” is the most important skill you can develop.

In this guide, we will break down the mechanics of both, explore the risks, and help you determine the perfect balance for your unique financial situation.

Understanding the Fundamental Difference: Safety vs. Growth

At its core, the difference between saving and investing comes down to intent and risk.

-

Saving is the act of putting money aside in highly liquid, low-risk accounts. The primary goal is preservation. You save because you want to ensure that if you put $1,000 away today, you will still have at least $1,000 tomorrow.

-

Investing is the act of using your money to purchase assets that you believe will increase in value over time or generate income. The primary goal is wealth creation. You invest because you want that $1,000 today to grow into $5,000 or $10,000 over the next decade.

Think of saving as your defense and investing as your offense. You need both to win the game, but they play very different roles on the field.

Defining Saving: The Importance of the Emergency Fund and Liquidity

Saving is the bedrock of financial security. In the United States, most savings are held in traditional savings accounts, High-Yield Savings Accounts (HYSA), or Certificates of Deposit (CDs).

Why We Save

We save for the “known unknowns.” Life is unpredictable, and savings provide the cushion that prevents a temporary setback from becoming a permanent financial disaster.

-

Emergency Funds: Ideally, you should have 3 to 6 months of living expenses saved in an account you can access instantly.

-

Short-Term Goals: If you plan to buy a house in two years, get married next summer, or buy a car in six months, that money belongs in a savings account.

-

Peace of Mind: There is a psychological value to “cash on hand” that cannot be measured in interest rates.

The Trade-Off: Low Returns

The cost of the safety and liquidity found in saving is the return. While interest rates on HYSAs in 2026 are more competitive than they were a decade ago, they rarely outpace the true cost of living by a significant margin.

Defining Investing: Harnessing the Power of Assets

Investing is where the magic of the global economy works for you. When you invest, you are taking a calculated risk that your capital will grow.

The Main Vehicles of Investment

-

Stocks (Equities): Buying a piece of a company.

-

Bonds (Fixed Income): Lending money to a government or corporation in exchange for interest.

-

Real Estate: Purchasing physical property or Real Estate Investment Trusts (REITs).

-

ETFs and Mutual Funds: Bundling hundreds of assets into a single purchase for instant diversification.

The Primary Goal: Beating Inflation

Investing is not just about “getting rich”; it is about maintaining purchasing power. If inflation is at 3% and your savings account pays 1%, you are technically losing money every year in terms of what you can actually buy. Investing is the only reliable way to ensure your money grows faster than the cost of bread, rent, and healthcare.

Risk vs. Reward: Navigating the Core Financial Trade-Off

Every financial decision involves a trade-off. In the world of finance, this is known as the Risk-Reward Profile.

| Feature | Saving | Investing |

| Risk Level | Minimal / Low | Moderate to High |

| Expected Return | Low (Interest) | Higher (Capital Gains/Dividends) |

| Liquidity | High (Instant access) | Moderate (May take days to sell) |

| Time Horizon | Short-term (0-3 years) | Long-term (5+ years) |

| Protection | Often FDIC insured | No guarantee of principal |

Pro Tip: Never invest money that you cannot afford to lose or money that you will need within the next three years. The stock market is a wealth-builder over decades, but a volatile roller coaster over days and months.

The Silent Killer: How Inflation Erodes Your Savings Over Time

Many people feel that investing is “risky,” but they fail to see the risk of not investing. This is the risk of Inflation.

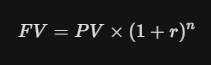

Inflation is the gradual increase in prices and the fall in the purchasing value of money. To understand the impact, consider the formula for the future value of money:

Where:

-

FV = Future Value

-

PV = Present Value

-

r = Annual inflation rate

-

n = Number of years

If you have $100,000 in a safe under your bed and inflation is at a steady 3%, in 20 years, that $100,000 will only buy what $55,367 buys today. By “saving” in a way that doesn’t earn a return, you have effectively lost nearly half of your wealth to the passage of time. This is why investing is a necessity, not an option.

The Magic of Compounding: Why Investors Win the Long Game

While savers earn simple interest (interest on the principal), investors benefit from compound growth (growth on the principal plus the growth from previous years).

This is often called the “Snowball Effect.” In the beginning, the growth is slow and almost unnoticeable. However, after 10, 20, or 30 years, the curve turns vertical.

The Rule of 72

To understand how fast your money will double when investing, use the Rule of 72:

-

At a savings rate of 1%, it will take 72 years for your money to double.

-

At an investment return of 8% (a historical average for the S&P 500), it will take only 9 years for your money to double.

Liquidity and Accessibility: When Do You Need Your Money?

Liquidity refers to how quickly you can turn an asset into cash without losing value.

-

Saving is High Liquidity: You can walk to an ATM or transfer funds from a HYSA to your checking account instantly. This makes saving perfect for “now” money.

-

Investing is Lower Liquidity: While you can sell a stock or an ETF during market hours, it often takes two business days for the funds to “settle” and be available for withdrawal. Furthermore, if the market is down when you need the money, you may be forced to sell at a loss. This is why you should never invest your rent money.

Identifying Your Investor Profile: Which One Are You?

Before deciding how to split your money between saving and investing, you must assess your Risk Tolerance and Time Horizon.

The Conservative Saver

Typically someone near retirement or someone with a very low tolerance for stress. They prioritize keeping what they have over growing it. They may keep 60% in savings/bonds and only 40% in stocks.

The Aggressive Investor

Typically a young professional with 30+ years until retirement. They see market crashes as “sales” and are happy to keep 90% of their wealth in equities, knowing they have time to recover from any downturn.

The Balanced Architect

The most common profile. They maintain a healthy emergency fund (saving) while consistently contributing to a diversified portfolio of ETFs and index funds (investing).

Opportunity Cost: The Hidden Price of Being Too Safe

In economics, Opportunity Cost is the value of what you give up when you choose one option over another.

If you choose to keep $50,000 in a savings account earning 1% instead of an index fund earning 8%, the “safety” of that account is costing you roughly $3,500 every single year in lost potential gains. Over 20 years, that “safety” could cost you over $150,000.

While you should always have an emergency fund, keeping excessive amounts of cash in a savings account is one of the most common mistakes beginners make. It feels safe, but it is actually a slow drain on your future wealth.

The 50/30/20 Rule: A Practical Framework for Your Budget

If you are unsure how to start, the 50/30/20 rule is a gold standard for personal finance:

-

50% for Needs: Rent, groceries, utilities, and insurance.

-

30% for Wants: Dining out, travel, and hobbies.

-

20% for Financial Goals: This 20% should be split between saving (until your emergency fund is full) and investing (for retirement and long-term wealth).

Once your “Needs” are met and your emergency fund is “Saved,” that entire 20% (or more!) should be funneled into “Investing.”

Common Myths About Saving and Investing

To make the best decisions, we must clear away the misinformation.

-

Myth 1: “Investing is just gambling.”

-

Truth: Gambling has a negative expected return (the house always wins). Investing in the global economy has a historically positive expected return as companies innovate and grow.

-

-

Myth 2: “I don’t have enough money to invest.”

-

Truth: In 2026, you can buy fractional shares. You can start investing with as little as $5.

-

-

Myth 3: “Saving is always the safest option.”

-

Truth: Saving is safe from “market crashes,” but it is certain to lose value to inflation over long periods.

-

Transitioning from Saver to Investor: A Step-by-Step Guide

If you have been a “saver” your whole life, moving into “investing” can be scary. Here is the logical path forward:

-

Check your debt: Ensure you have no high-interest credit card debt.

-

Fill your bucket: Build a 3-month emergency fund in a High-Yield Savings Account.

-

Start small: Open a brokerage account and buy $50 of a “Total Market ETF” like VTI or VOO.

-

Automate: Set up a monthly transfer. Treat your investment like a bill that you pay to your “future self.”

-

Educate yourself: Read books like The Simple Path to Wealth or The Intelligent Investor.

Balancing Your Financial Ecosystem

Saving and investing are not rivals; they are partners. Saving gives you the security to sleep at night, and investing gives you the wealth to live the life you want in the future.

The most successful people in the world of finance are those who have mastered the “buffer” of savings so they never have to touch their “engine” of investments. By filling your savings bucket first and then aggressively filling your investment bucket, you are setting yourself up for a future where you don’t work for money—money works for you.

Start your emergency fund today, but don’t let your money sit idle forever. The market is open, and the power of compounding is waiting for you.