Why do people spend where they don’t have it?

Understand the emotional triggers behind excessive consumption

We have all been there. You open your banking app or a credit card statement at the end of the month, and your heart sinks. You see a number that doesn’t quite align with the reality of your paycheck. For many, this isn’t a one-time mistake but a recurring cycle. In an era of “Buy Now, Pay Later,” one-click ordering, and social media influencers showcasing a life of perpetual luxury, the phenomenon of spending money we don’t have has become a global epidemic.

But why do we do it? Is it a lack of willpower, or is there something deeper at play in our biology, our upbringing, and our culture? Understanding the “why” behind overspending is the first and most critical step toward breaking the cycle and achieving genuine financial freedom. This deep dive explores the psychological traps, marketing manipulations, and economic factors that lead us to spend beyond our means.

The Biological Hook: Dopamine and the “Reward” of a Purchase

To understand overspending, we must first look at the human brain. We are wired for survival, and for most of human history, “getting” was synonymous with “surviving.” When our ancestors found a beehive or a berry bush, the brain released dopamine—a neurotransmitter associated with pleasure and reward—to encourage that behavior.

The Dopamine Loop in Modern Shopping

In 2026, we don’t hunt for berries; we hunt for deals. When you click “Place Order” or swipe your card for a new gadget, your brain experiences a significant dopamine spike. This chemical “high” is most intense during the anticipation phase. Interestingly, the pleasure often peaks before you even have the item in your hands.

Once the item arrives and the novelty wears off, the dopamine levels crash. To get that feeling back, the brain craves another transaction. This creates a loop of “Retail Therapy” where we spend not because we need the item, but because we are subconsciously self-medicating for stress, boredom, or sadness.

The “What-the-Hell” Effect

Psychologists use the term “What-the-Hell Effect” to describe a cycle of indulgence, regret, and further indulgence. If you blow your budget by $50 on a Friday night, your brain might say, “Well, the budget is already ruined, so what the hell, I might as well buy that $200 jacket too.” This all-or-nothing thinking is one of the quickest ways to fall into deep consumer debt.

The Invisible Cost: How Frictionless Payments Mask the Pain of Paying

In the days of physical currency, spending money hurt. When you had to physically count out five $20 bills and hand them to a cashier, your brain registered a “loss.” This is what behavioral economists call the “Pain of Paying.”

The Elimination of Friction

Modern financial technology is designed to eliminate this pain. Every innovation—from credit cards and Apple Pay to FaceID and “One-Click” ordering—is a move toward frictionless spending.

-

Credit Cards: You aren’t losing money; you are gaining a product and “delaying” the consequence.

-

Biometrics: A thumbprint or a face scan is so fast that the analytical part of your brain (the prefrontal cortex) doesn’t have time to intervene.

-

Buy Now, Pay Later (BNPL): Services like Affirm or Klarna break a $400 purchase into four “easy” payments of $100. Your brain perceives the cost as $100, not $400, lowering your psychological defenses.

Digital Disconnection

When money is just a digital number on a screen, it feels less “real.” This disconnection makes it incredibly easy to spend money you haven’t earned yet because you don’t feel the immediate weight of the loss. You are effectively borrowing from your “future self” to satisfy your “current self.”

Social Comparison and the “Instagram” Distortion of Wealth

As social animals, our status within the tribe used to be a matter of life and death. Today, status is signaled through consumption. This leads to the age-old problem of “Keeping up with the Joneses,” but with a dangerous modern twist.

The Curated Reality

In the past, you only compared yourself to your neighbors. Today, you compare your “behind-the-scenes” reality to the “highlight reels” of everyone else in the world. When you see influencers or even your friends posting about their new cars, designer clothes, and five-star vacations, you experience FOMO (Fear Of Missing Out).

What you don’t see is the credit card debt, the leased vehicles, or the fact that the “luxury” hotel room was paid for with points or is being subsidized by a high-interest loan. We spend money we don’t have to maintain an image of a life we can’t afford, all to impress people who are likely doing the exact same thing.

Status Anxiety

Status anxiety is the constant fear that we are perceived as “unsuccessful” by our peers. In a consumerist society, we use brands as a shorthand for our value. We buy the expensive brand of coffee or the latest smartphone not because they are functionally superior, but because they signal that we are “winning” the game of life.

Marketing Manipulation: The Science of Creating Artificial Urgency

You aren’t just fighting your own impulses; you are fighting some of the world’s most powerful AI and marketing algorithms. Retailers spend billions to understand exactly how to trigger your “buy” response.

Artificial Scarcity and “Dark Patterns”

Ever seen a countdown timer on a website saying “Sale ends in 02:14:55”? Or a notification that “14 other people are looking at this item”?

These are often manufactured to trigger a sense of panic. When we perceive scarcity, our “fight or flight” response kicks in. The fear of losing the deal becomes more powerful than the rational need for the item.

The “Anchor” Effect

Retailers often list a “MSRP” or “Original Price” that is significantly higher than the current price. Your brain “anchors” on that high number. Even if the sale price is still expensive, you perceive it as a “win” or “saving money.” You aren’t saving money; you are spending money you wouldn’t have spent otherwise.

The Identity Trap: Spending to Become the Person We Want to Be

One of the most profound reasons we spend money we don’t have is to bridge the gap between who we are and who we want to be. We don’t buy products; we buy “versions of ourselves.”

-

You buy the $2,000 Peloton because you want to be “a fit person.”

-

You buy the expensive kitchen gadgets because you want to be “a gourmet chef.”

-

You buy the high-end camera because you want to be “a creative photographer.”

We often mistake the acquisition of the tool for the mastery of the skill. We spend the money as a shortcut to an identity, but when the excitement fades and the debt remains, we realize that the identity required work, not just a credit card.

The Economic Reality: The “Vimes’ Boots” Theory of Inequity

It is important to acknowledge that not all overspending is fueled by vanity or impulse. For many, spending money they don’t have is a matter of survival in an economy where wages have not kept pace with inflation.

The Cost of Being Poor

Author Terry Pratchett famously described the “Vimes’ Boots Theory of Socioeconomic Unfairness.” A wealthy person can buy a $50 pair of boots that lasts ten years. A poor person can only afford $10 boots that last a season. Over ten years, the poor person spends $100 on boots and still has wet feet, while the wealthy person spent $50 and has dry feet.

When people lack a “cushion,” they often have to use credit to cover emergencies—a car repair, a medical bill, or an appliance failure. Once you are in the cycle of high-interest debt, it is mathematically difficult to escape, leading to a life where you are perpetually spending money you haven’t earned yet just to stay afloat.

Lack of Financial Literacy: The “Minimum Payment” Trap

The financial system is complex, and it is not always designed to favor the consumer. Many people spend money they don’t have because they don’t fully understand the “math of debt.”

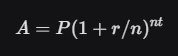

The Power of Compound Interest (in Reverse)

While compound interest is a miracle for savers, it is a nightmare for debtors.

If you have a $5,000 balance on a credit card with a 24% APR and you only pay the “minimum payment,” it will take you over 20 years to pay it off, and you will end up paying more than $10,000 in interest alone.

Most people see a “Minimum Payment” of $120 and think they are “handling” their debt. In reality, they are barely covering the interest, ensuring they stay in debt for a generation. The lack of clear education on how interest works is a primary reason people feel comfortable spending money that isn’t theirs.

How to Break the Cycle: Actionable Steps to Financial Sovereignty

If you find yourself caught in the cycle of spending money you don’t have, the solution isn’t just “more money.” It is a change in system and mindset.

1. Re-introduce Friction

The easier it is to spend, the more you will spend.

-

Delete shopping apps from your phone.

-

Remove saved credit card info from your browser.

-

Use the “72-Hour Rule”: For any purchase over $50, wait three days. Usually, the dopamine fades and you realize you don’t need it.

2. Track Your “Net Worth,” Not Your “Balance”

Your bank balance is a snapshot of what you have; your net worth is a snapshot of your reality. Use a simple spreadsheet or an app to track your total assets vs. your total liabilities (debts). Seeing that “Debt” number shrink is a much more powerful reward than buying a new shirt.

3. Identify Your Triggers

Are you a “Stress Spender”? Do you shop when you’re bored at 11 PM? Once you identify the emotional trigger, you can replace the “Routine.” Instead of opening a shopping app when stressed, try a 10-minute walk or a workout. You get the dopamine without the debt.

4. Build a “Starter” Emergency Fund

The first step out of debt is to stop getting into more debt. Save $1,000 as fast as you can. This is your “buffer.” When the tire blows or the phone breaks, you pay for it with your own money instead of a high-interest credit card.

Wealth is Not What You Spend, It’s What You Keep

In a world that profit from your impulsivity, the most radical act you can perform is to be content with what you have. Spending money you don’t have is a form of self-sabotage that steals your future freedom for a temporary, chemical high.

True wealth isn’t about the car you drive or the brand on your back; it’s about the security of knowing you owe no one, the freedom to leave a job you hate, and the peace of mind that comes from being in total control of your resources. Stop being a spectator in the “status game” and start being the architect of your financial future.