When you apply for a loan, the lender provides you with a set of numbers that can often feel like a foreign language. You see terms like “Principal,” “APR,” “Compound Interest,” and “Amortization.” While it’s tempting to simply look at the monthly payment and sign on the dotted line, understanding how those numbers are calculated is the most powerful tool you have as a consumer.

Calculating loan interest isn’t just a task for mathematicians or bankers. It is a fundamental life skill that allows you to compare different financial products accurately, plan your monthly budget, and ultimately save thousands of dollars over your lifetime. In this guide, we will strip away the complexity and show you exactly how loan interest works, how to calculate it yourself, and what “hidden” factors influence the total price of your debt.

The Core Components: Understanding the Vocabulary of Lending

Before we dive into the math, we need to define the variables. Every loan calculation relies on four primary pieces of information.

The Principal Amount

This is the total amount of money you are borrowing. If you take out a $10,000 personal loan to consolidate debt, $10,000 is your principal. As you make payments, a portion goes toward reducing this balance.

The Interest Rate

This is the percentage of the principal that the lender charges you for the privilege of using their money. It is usually expressed as an annual figure (e.g., 7% per year).

The Loan Term

This is the length of time you have to pay the loan back (e.g., 3 years, 5 years, or 30 years for a mortgage). The longer the term, the more interest you will pay in total, even if the monthly payments are lower.

The Repayment Frequency

Most loans are repaid monthly, but some may be bi-weekly or quarterly. The frequency affects how often interest is calculated and applied to your balance.

Simple Interest vs. Compound Interest: What’s the Difference?

Not all interest is calculated the same way. Depending on the type of loan you have, the math can change significantly.

Simple Interest Calculation

Simple interest is the most straightforward method. It is calculated only on the principal amount. You often see this with short-term personal loans or private loans between individuals.

The formula for simple interest is:

For example, if you borrow $5,000 at a 6% simple interest rate for 2 years:

Your total repayment would be $5,600.

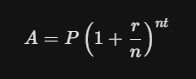

Compound Interest Calculation

Compound interest is more common in the banking world (especially for credit cards and some mortgages). This is “interest on interest.” The interest is calculated on the principal plus any interest that has already accumulated.

The formula for compound interest is:

-

A = the total amount (principal + interest)

-

P = the principal amount

-

r = annual interest rate (decimal)

-

n = number of times interest compounds per year

-

t = time in years

Compound interest grows faster than simple interest, which is why credit card debt can spiral out of control so quickly if only minimum payments are made.

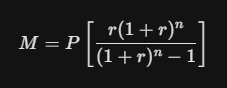

How to Calculate Your Monthly Loan Payment Using Amortization

Most personal loans, auto loans, and mortgages use a process called amortization. This means you make fixed monthly payments, but the ratio of interest to principal changes every month. In the beginning, most of your money goes toward interest. Toward the end of the loan, most of it goes toward the principal.

To calculate the monthly payment (M) for an amortized loan, use this formula:

-

P = Principal loan amount

-

r = Monthly interest rate (Annual rate divided by 12)

-

n = Number of months (Term years multiplied by 12)

Why This Matters to You

Understanding amortization helps you realize why “paying a little extra” early in the loan is so effective. By reducing the principal faster in the early stages, you prevent a massive amount of future interest from ever being calculated.

The APR Trap: Why the Interest Rate Isn’t the Whole Story

When comparing loans, you will see two numbers: the Interest Rate and the APR (Annual Percentage Rate).

The interest rate is just the cost of the principal. The APR includes the interest rate plus any mandatory fees (origination fees, processing fees, etc.).

Example:

-

Loan A: 5% interest rate + $500 in fees.

-

Loan B: 5.5% interest rate + $0 in fees.

On a small, short-term loan, Loan B might actually be cheaper, even though the interest rate is higher. Always use the APR to compare the true cost of borrowing.

How Daily Interest Accrual Works

Most modern personal loans and student loans use a daily interest model. This means the lender calculates how much interest you owe every single day based on your current balance.

To find your daily interest charge:

-

Take your annual interest rate (e.g., 12% or 0.12).

-

Divide by 365 (0.12 / 365 = 0.00032).

-

Multiply by your current balance ($10,000 \times 0.00032 = \$3.20$).

In this example, you are being charged $3.20 in interest every day. If you pay your bill five days early, you save five days’ worth of interest ($16.00). If you pay five days late, you owe an extra $16.00 in interest alone, on top of any late fees.

Fixed vs. Variable Rates: Calculating the Risk

When you calculate your interest, you must know if your rate is Fixed or Variable.

-

Fixed Rate: The rate never changes. Your calculation today will be accurate until the loan is paid off.

-

Variable Rate: The rate is tied to an index (like the Prime Rate). If the index goes up, your interest rate goes up.

When calculating a variable rate loan, always perform a “stress test.” Calculate what your monthly payment would be if the interest rate rose by 2% or 3%. If that new number breaks your budget, a variable rate loan is too risky for you.

The Impact of Loan Terms on Total Interest Paid

One of the biggest mistakes borrowers make is focusing only on the monthly payment. Lenders often encourage longer terms (like 72 or 84 months for a car) because it makes the monthly payment look “affordable.”

However, look at the total interest on a $20,000 loan at 8%:

-

3-Year Term: Total Interest = $2,544

-

6-Year Term: Total Interest = $5,184

By doubling the length of the loan to get a lower payment, you are paying double the interest. Always choose the shortest term that your monthly budget can comfortably handle.

Avoiding “Add-on Interest” Loans

Be very wary of lenders who use “add-on interest.” In this model, the total interest for the entire term is calculated at the beginning and added to the principal. Even if you pay the loan off early, you still owe the full amount of interest. This is much more expensive than the standard declining-balance interest used by most banks and credit unions. Always ask your lender: “Is this a simple interest, declining-balance loan?”

How to Use Online Loan Calculators Effectively

While doing the math by hand is educational, online calculators are faster and reduce the risk of error. When using a calculator:

-

Input the APR, not just the base interest rate.

-

Check for an Amortization Schedule. This shows you exactly how much of each payment goes to principal vs. interest.

-

Experiment with Extra Payments. Most good calculators allow you to see how much time and money you save by adding an extra $50 or $100 to your monthly payment.

Knowledge is Financial Power

Calculating loan interest is about more than just numbers—it’s about seeing the “true price” of the things you buy. When you know how to calculate your own interest, you stop being a passive borrower and start being a savvy financial manager. You can spot bad deals, avoid predatory fees, and choose the repayment strategy that keeps the most money in your pocket.

Before you take out your next loan, take ten minutes to run the numbers yourself. You might be surprised at what you discover.